The Bull Case for Polaris

Polaris spent two years building fully onchain, counterparty-free infrastructure while others wrapped TradFi yield. Here's what that leads to.

The Bull Case for Polaris

We've covered the core mechanisms. Now let's talk about what they add up to — and why Polaris is positioned to become core infrastructure for DeFi.

Stablecoins have the clearest product-market fit in crypto. Citi projects the sector growing from over $300 billion today to $4 trillion by 2030. Yet the largest centrally-issued stablecoins share the same fundamental weakness: a single issuer who can freeze your funds. And the vast majority of stablecoin yield traces back to offchain sources, whether T-bills, CEX lending, or custodial strategies.

The pattern is familiar. When the easy path exists — wrap some offchain yield, raise millions from investors, launch a token at an inflated valuation — that's the path most will take. We've seen it play out with hundreds of stablecoin issuers bringing wrapped hedge fund strategies and RWAs to market, calling them "stablecoins" and racing to accumulate TVL.

DeFi users should not be TradFi's exit liquidity. We can do much better than this.

Innovating is hard

Those of us around during DeFi Summer remember those times fondly. It seemed like every single day, sometimes multiple times a day, something innovative was launching. Extremely high yields, new game theory to figure out, novel primitives that forced you to actually think. DeFi was at the cutting edge of crypto innovation, and some of those experiments became household names with some of the clearest product-market fit in the industry.

Since then, innovation has slowed significantly. The low-hanging fruit has been discovered and tested, and many of the simplest mechanisms had too many extraction paths for sophisticated participants to exploit. But the fact that the most obvious approaches couldn't scale doesn't mean we've discovered every fully onchain, DeFi-native primitive that can let this industry stand on its own two feet, untethered from TradFi.

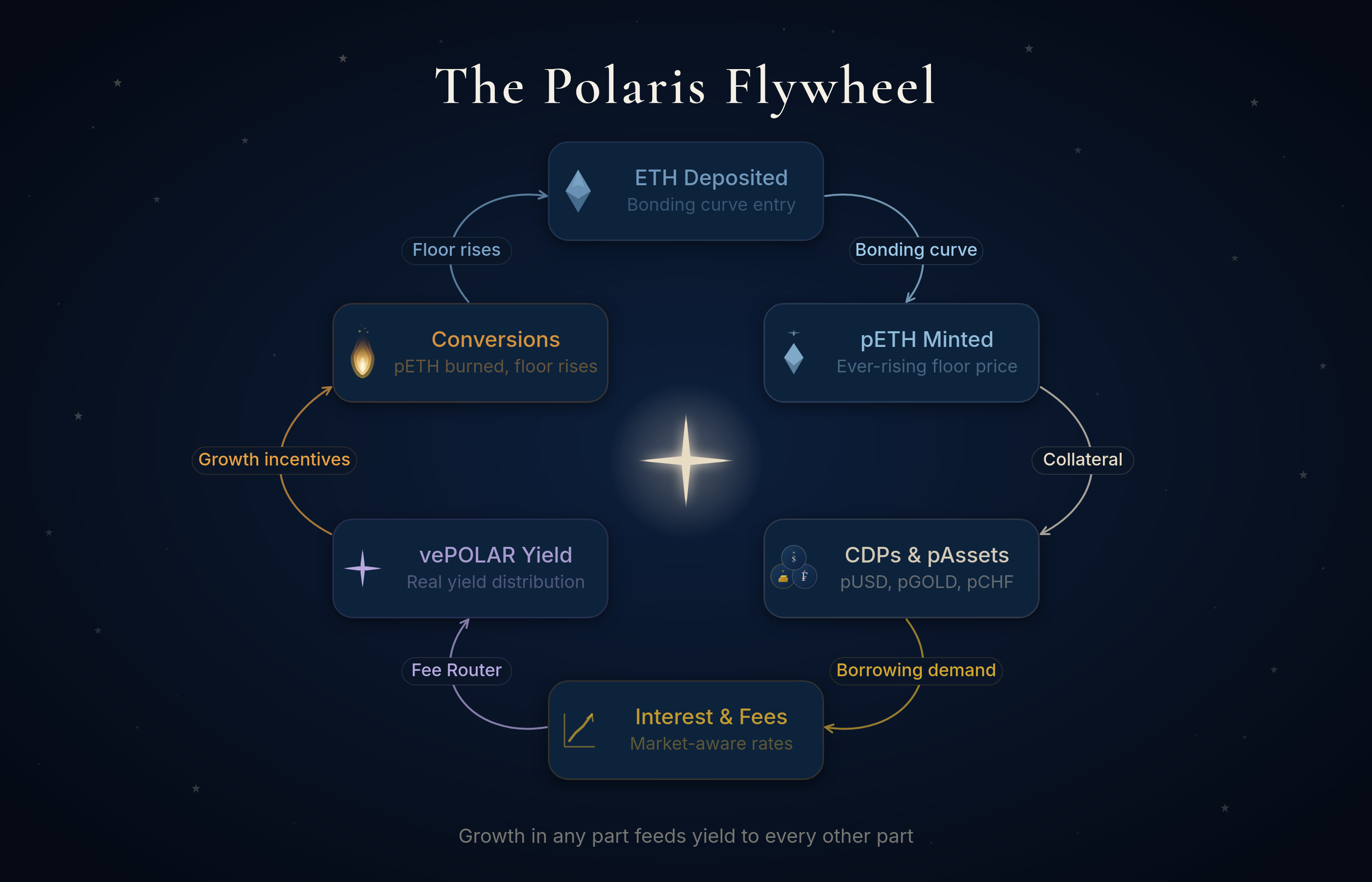

Almost two years ago, Polaris set out to answer that question — not with a thesis deck, but with mechanism design. The bonding curve gave pETH an ever-rising floor price without external liquidity providers. The CDP architecture produced autonomous, market-aware interest rates instead of governance-set ones. The conversion mechanism aligned POLAR's token economics with protocol health rather than speculation. Each was the harder path — and each was chosen deliberately while the rest of the market was busy wrapping offchain yield.

This is not the "sexy" path. Many doubt whether fully onchain, decentralised, counterparty-free DeFi can actually scale, or whether the market even cares. Others question whether the mechanisms are too complex for users. We've even been asked "where do you park the liquidity to earn yield for your stablecoin?" by investors who assume that generating yield without wrapping TradFi is no longer possible.

We'll take the hard path. Here's what it leads to.

Polaris is the North Star for Ethereum

Vitalik has recently become vocal about stablecoins, posting on X that decentralised stablecoins face three problems:

- Figuring out an index to track that's better than the USD price

- Oracle design that's decentralised and not capturable with a large pool of money

- Solving the problem that staking yield is competition

Polaris directly solves points 1 and 3. More robust oracle design is something the entire industry needs to work towards, but the Polaris oracle architecture minimises oracle surface area to the absolute minimum. For pUSD, that means just the ETH/USD price feed, from which the pETH price can be derived. pUSD itself doesn't need a separate USD oracle because its price is derived from minting and redemption volume.

Let's zoom in on the two points we solve.

Figuring out an index to track other than USD

For anyone not denominating in USD — which is most of the world — holding dollar-pegged stablecoins onchain has not been kind over recent months. And all central banks are inflating their currencies into oblivion; forex swings will continue to wreak havoc on investors.

DeFi, and more specifically the Polaris infrastructure, allows us to move the unit of exchange away from USD and into any index we want to track. This is possible because Polaris can facilitate negative real rates: it incentivises borrowers in proportion to their debt with pETH fees, which allows the protocol to mint any synthetic asset. All you need is an oracle feed that determines the price of that asset.

pEUR. pCHF. pGOLD. pBigMac. These assets all inherit the same properties that Polaris provides: decentralised, no counterparty exposure, yield-bearing, and fully onchain, backed by Ethereum. The StablecoinOS is not just a stablecoin protocol. It's a synthetic asset factory that can mint any yield-bearing asset you desire.

Solving the problem of staking yield as competition

This is where the bull post grows horns.

So far, most people know Polaris for the StablecoinOS: a completely uncorrelated yield source powering a CDP protocol that is immutable and counterparty-free. But the CDP protocol is the trojan horse for what we believe is the true potential of Polaris — and the reason we spent two years building it.

One of our internal visions is pETH as the default reserve asset across DeFi. This plays directly into Vitalik's third point: in its current form, ETH staking represented as a token doesn't suit itself as collateral for a fully decentralised stablecoin.

pETH, on the other hand, is an entirely new asset designed specifically for this use case. It also has other interesting properties: an ever-rising floor price combined with additional volatility along the bonding curve that allows it to draw liquidity away from ETH staking directly (see The Bonding Curve: Polaris' Secret Weapon for more on pETH).

Splitting pETH? The assets DeFi doesn't know it needs yet

Here's where it gets interesting. It's possible to split pETH's two properties — floor price and volatility — similar to how Pendle splits yield-bearing tokens into PT and YT. This creates two very compelling new assets:

fpETH — represents the floor price of pETH. An up-only ETH token directly comparable to LSTs like wstETH. It earns yield as the floor price moves up the bonding curve, capturing all bonding curve trading volume and pETH → POLAR conversions. No slashing risk, no withdrawal queue, no downside risk. It's directly redeemable against the protocol by combining one fpETH and one vpETH to redeem one pETH.

Why is fpETH yield structurally different from staking? Because its yield is driven by bonding curve trading activity and conversion volume — two fee sources that scale with protocol adoption rather than being capped by Ethereum's issuance schedule. Every new pAsset minted, every conversion, every trade along the curve feeds the floor price. The more the protocol is used, the faster the floor rises.

vpETH — represents the volatile component of pETH that sits above the floor price. More risky than fpETH, but it allows holders to speculate on and gain additional exposure to pETH/ETH volatility. Critically, it also allows stablecoin minters to hedge the pETH volatility of their position and run delta-neutral stablecoin backing strategies on top of Polaris.

The fpETH/vpETH split is in active research and design. But even without the split, pETH already offers a yield profile that is completely uncorrelated to staking, censorship-resistant, and fully Ethereum-aligned. fpETH and vpETH sharpen this into specialised instruments that can serve distinct audiences: conservative treasuries, yield-seeking protocols, and sophisticated hedgers alike.

None of this is possible without the CDP protocol driving deposits into the bonding curve in the first place. And every future product built on top of pETH and the bonding curve is designed to drive value back to pUSD, all pAssets, and POLAR. The flywheel is intentional.

What this means for POLAR

If pETH becomes core DeFi infrastructure, POLAR is the coordination layer for protocol growth.

Every pETH → POLAR conversion burns pETH and sends ETH through the Fee Router to trove depositors. More pETH demand means more bonding curve activity, which means more conversion volume. The constant floor increases of pETH, along with its yield while deployed in a CDP, result in higher borrowing demand, translating into higher revenues for vePOLAR which capture some of the interest rate. The mechanism is circular by design: growth in any part of the system feeds yield to every other part.

vePOLAR lockers don't just earn fees — they steward the protocol's parameters within hardcoded bounds such as setting converter rebates, or licensing new pAssets via StablecoinOS. This is real, bounded utility — not a governance token searching for a reason to exist.

As StablecoinOS scales and more pAssets are minted, fee volume grows across every bonding curve and every CDP. That fee activity flows through the protocol's tokenomics via POLAR. The bull case for Polaris is the bull case for POLAR — they are the same flywheel.

The institutionalisation of DeFi

The suits are here and institutional adoption is happening, but the flow is mostly one way. We have an influx of new RWAs entering DeFi, institutions figuring out how to sell their products to DeFi investors, and a broader push to tap into DeFi liquidity that is generally more risk-tolerant than capital within traditional finance.

The flow in the other direction has been much slower. While institutions want to sell to DeFi, they remain wary of DeFi counterparty risk, and honestly, we can't blame them. This industry has repeatedly demonstrated its inability to manage risk and that many of its participants are not counterparties worth trusting. Institutions will only trust regulated counterparties in their own jurisdictions — or even better, they won't have to trust a counterparty at all.

This is where the pieces connect. An asset like fpETH — up-only, no counterparty, no withdrawal queue, redeemable against audited, immutable smart contracts — is precisely the kind of instrument a treasury or fund can hold without trusting a team, a multisig, or a jurisdiction. It offers yield that doesn't exist in traditional finance, delivered through a protocol that can't change the rules after you deposit.

This is also why Ethereum's focus on decentralisation and censorship resistance matters. It makes Ethereum the only logical base layer for a protocol that prioritises these same properties. You are only as robust as the chain you build on.

When we think about scaling DeFi to the world — not just the United States but the entire world — this can only be done using a completely decentralised, immutable, and counterparty-free protocol. Only a handful of protocols in this industry can make that claim.

The bear case we take seriously

We wouldn't be Polaris if we didn't address the hardest criticisms head-on. Let's cover the most recurring ones:

"Immutability means you can't fix bugs." This is the sharpest trade-off we've made, and we accept it with open eyes. No upgrade path means no governance capture, no parameter manipulation, no slow drift toward centralisation — but it also means the code must be right before deployment. This is why we've spent nearly two years in development rather than rushing to market. Immutability is a feature, but only if you earn it through rigorous auditing. We take that seriously.

"fpETH/vpETH is still in research — are you building a bull case on vapour?" Fair question. The bull case for Polaris does not depend on fpETH/vpETH shipping. fpETH/vpETH is an additive design that will likely make the cut, but still, pETH already works as a standalone asset with an ever-rising floor and uncorrelated yield. The split is an amplifier, not a prerequisite. If it ships, it expands pETH's addressable market dramatically. If it requires more research time, the core protocol delivers on its own.

"The flywheel needs a cold start." Every protocol faces the bootstrapping problem, and we won't pretend otherwise. The bonding curve needs initial deposits; the CDP needs initial borrowers; the conversion mechanism needs pETH supply to burn. Our approach is to let the mechanism design do the work: the bonding curve structurally incentivises early depositors with higher yield per unit of capital, and the arbitrage loops that maintain the peg create organic demand from day one. But yes — the first months will be the hardest and we are preparing for them on all fronts, business development included. We're also building for what comes after.

"The mechanisms are too complex for most users." Complexity under the hood is not the same as complexity for the user. You don't need to understand the bonding curve to deposit ETH and earn yield. Abstractions exist precisely so that users can interact with simple interfaces while the protocol handles the rest. That said, we believe DeFi deserves protocols worth understanding — and the community we're building is one that values depth over simplicity.

The North Star

Polaris can only be built on Ethereum. And Ethereum will win because protocols like Polaris can only be built on Ethereum.

This post is for informational purposes only and does not constitute financial, investment, or legal advice, nor an offer or solicitation to purchase any token or financial instrument.

Follow Polaris on Twitter and join the Telegram announcement channel to not miss any news. You can also subscribe to the RSS feed if that is your thing.